2018 is likely to be a year where trade is caught in the cross-fire between isolationism in the US, Brexit in the UK and multilateralism in the rest of the world.

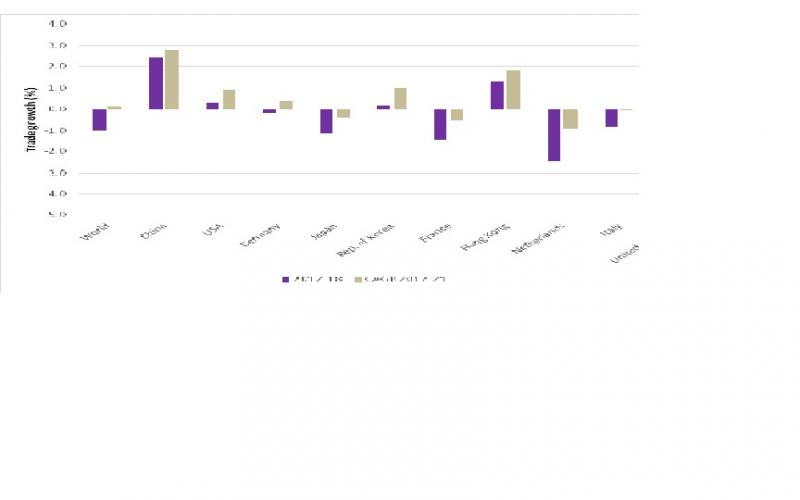

The difficult environment for trade in value terms is likely to continue during 2018. Although oil prices are likely to rise, and inflationary pressures set to build in Europe and the UK, this will still be insufficient to create a strong increase in the value of world trade during the course of the coming year. We expect world trade value growth to be flat or negative and for many countries to follow this pattern. (Figure 1). The only exception is the UAE which may show substantially increased trade in 2018 on the back of the oil price recovery and a diversion of trade from riskier countries in the region.

Figure 1: World trade growth by country, 2017-18 (%) and CAGR, 2017-21 (%)

Source: Coriolis Technologies 2018

NOTE: Projections are based on long and short term momentum and do not make assumptions about GDP, freight costs, or any future trade negotiations

This picture of trade is very much more negative than that of the World Trade Organisation (WTO). There are two reasons for this. First, the WTO bases its forecasts on volumes rather than values. Thus, while we may see volumes of trade increase, its real value may not increase – either because of inflationary pressures or because the US dollar remains comparatively weak. Second, the WTO picture is often over-optimistic, and its estimates of global volume growth of 3.6% in 2017 made last July already look awry in the light of flat trade towards the end of the year. The WTO is itself forecasting slower trade growth globally in 2018 of 3.2% and the value projections show a similar decline on last year (Figure 2).

Figure 2: World Trade and WTI spot price (average monthly), January 2010-Dec 2017

World trade values and oil prices have slowed markedly since mid 2014. Since the correlation between the value of global trade and the WTI spot price is high at 78%, this is unsurprising. Oil prices started to recover at the end of 2017 and this may help the value of trade to grow during the course of the year. However, even during periods of sustained growth in oil prices, for example in early 2015, the long-term effect on trade values has not been affected.

Risks to the forecast

In 2017 we predicted that the year would be dominated by the politics of trade. Our views have not changed and 2018 is likely to be a year where trade is caught in the cross-fire between isolationism in the US, Brexit in the UK and multilateralism in the rest of the world. There is no sign that multi-lateral agreements, say the Trans-Pacific Partnership (minus the US) will falter and similarly Brexit has offered an opportunity for Europe to reform and to tighten its single market over time.

Yet there is little doubt that the weaponised language around trade that was the feature of 2017 will abate. The US will threaten stronger tariff regimes, particularly against China, but the risks of an all-out Trade War are low given the relative weakness of the US compared to China in trade terms and, more importantly, the fact that Russia and China agreed closer ties at the start of the year which will strengthen China’s “one belt one road” initiative and create closer integration in the Eurasia region.

The Middle East’s trade during the course of the year will be driven by two things: first, the oil price itself and, perhaps more significantly, tensions in the region. If the oil price stabilises at a higher level, say $60 per barrel during the course of the year, then this helps to restore the economic health of some of the oil exporters in the region, and particularly Saudi Arabia. However, any economic recovery will not mask the tensions in the region which have spilled over into trade: the blockade of Qatar shows no signs of ending and the UAE is benefitting from that. Egypt, paradoxically perhaps, is part of the blockade but alongside that support is also increasingly trading with Russia and Iran, as is Oman. The geopolitical tensions have the potential to affect both the oil price and the nature and security of trade through the region.

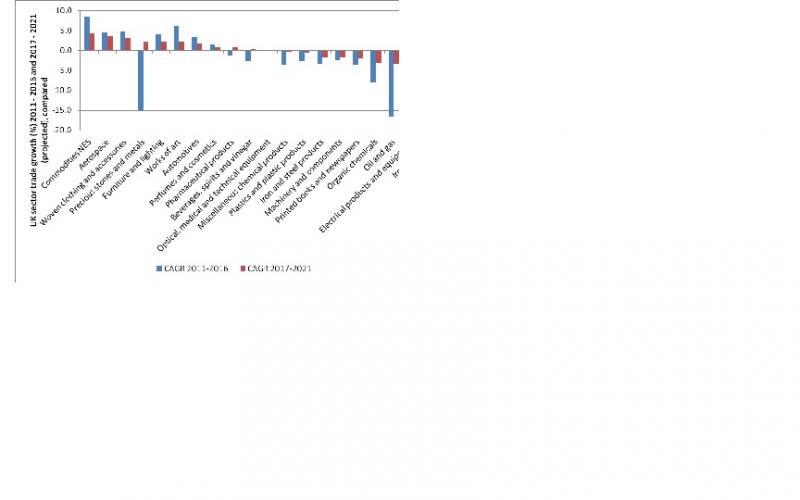

Finally, the UK’s trade picture over the next five years will be defined by the discussions that take place between the European Union and the UK’s negotiators during the course of the year. The UK’s economy is one of the more open of the G20 – the value of total trade (exports plus imports) is 58% of GDP.

Figure 3: UK trade growth rates compared, 2011-16 and 2017-21 (projected), (CAGR, %)

Figure 3 focuses just on goods trade, which is 52% of the value of the UK’s total trade. Based on momentum projections which assume nothing about the nature of the negotiations, the picture is one of weak growth in trade values beyond 2017. Ironically, this may be because of sterling’s current strength, which makes exported goods cheaper in US dollar terms. But although the growth is strong in some sectors, the growth in the largest export sectors (automotives, electrical equipment, machinery and components and pharmaceuticals for example) is projected to be negative over the next five years.

Overall then, it is likely to be the politics that determine the downside, or indeed the upside, risks of this forecast. That makes the world, and the trade world in particular, an uncertain, potentially dangerous but interesting place.

Dr Rebecca Harding, Liveryman

CEO, Equant Analytics

Women in FinTech Powerlist, 2017: http://womeninfintech.co.uk/wp-content/uploads/2017/11/wif_2017_powerlist.pdf

Email: rh@equant-analytics.com

Tel: +44-(0)7803-710711

Twitter: @RebeccaAHarding

Skype: rh.equantanalytics

“The Weaponization of Trade: the Great Unbalancing of Politics and Economics”

Rebecca Harding and Jack Harding.

October 25th 2017 * 170pp paperback *£9.99

ISBN 978-1-907994-72-2

ORDER HERE: http://londonpublishingpartnership.co.uk/weaponization-of-trade/